Overview: This post illustrates Photon’s document uploads capabilities, namely creating unified summaries from multiple files spanning hundreds of thousands of words and obtaining aspect based summaries as well.

Consider topics of pressing interest like Inflation, Interest Rates, GDP Growth, Recession, etc. Officials in the financial services industry often spend hours (or days in fact) reading reports such as those from this post, trying to obtain pertinent insights. Unfortunately, the length of those linked articles rivals that of “Harry Potter and the Deathly Hallows” (minus the riveting plot twists), and treasure troves of data will likely just be ignored (unless a decision maker assigns the task of reading said reports in their entirety to a disgruntled intern, who ends up imploding and embezzling funds from the institution due to the dull and tedious nature of the task).

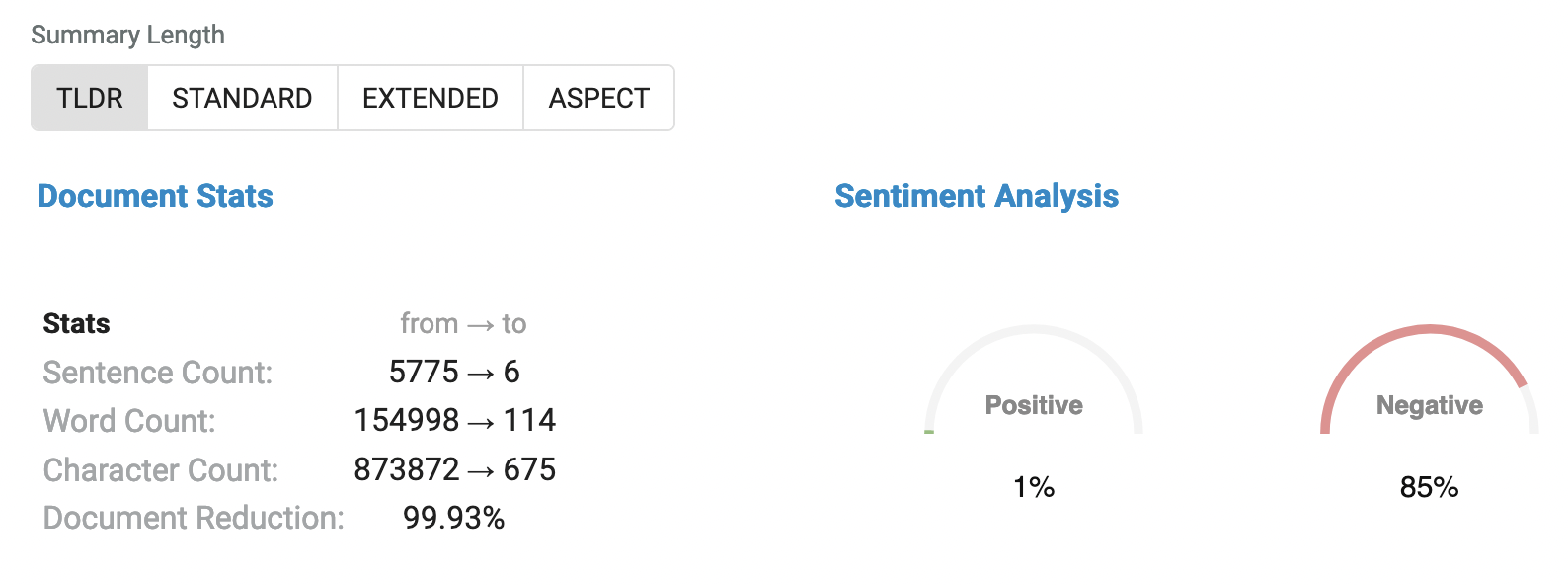

First, imagine one wants just the punchlines of all the linked articles. Below we see a unified TLDR of all the documents (this is very far from perfect, one could argue it’s too much compression to go from 155K words to 100, i.e., akin to explaining Harry Potter in 6 sentences, but note on our platform, we allow users to select lengths based on their preferences/desired compression levels) – all the summaries you’ll see below are completely AI generated (to understand a bit more of our summary process, please see this post- High level summarization methodology!

Photon Result (TLDR):

- The 2023 Outlook for investors is a recession, recovery, and rebound. Equity and bond benchmark indexes posted negative returns this past year due to high inflation and the end of pandemic-related transfer payments. Goldman Sachs Global Economics Analyst Exhibit 18 shows that the unvaccinated elderly remain at serious risk of severe outcomes. Central banks in Europe and those EM economies are still increasing and may be forced into further tightening. Equity valuations are yet to reflect the damage ahead, with the US entering a mild recession. The UN expert group has reported that one-third of the world’s largest publicly-traded businesses have made net zero commitments.

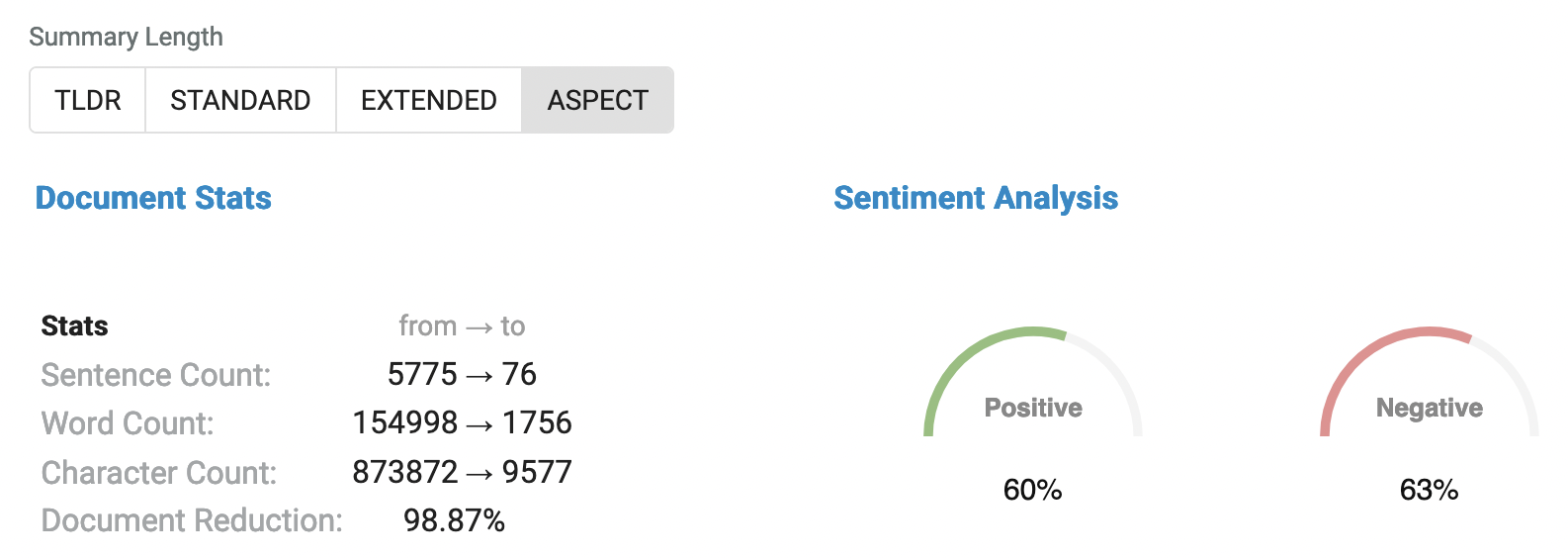

Next, consider wanting to know the outlook on Inflation, Interest Rates and GDP Growth based on all of the market outlooks. Photon Insights reads through all the articles in their entirety, and provides end users with unified insights on desired aspects. As seen below, Photon sifted through 155K words to provide a tractable < 2000 word summary, specifically focused on the queries aspects!

Photon Result (aspects = Inflation, Interest Rates, GDP Growth)

- The US experienced an asset bubble-induced recession in 2001, but the US dollar continued to rise through much of 2002. This was despite sharp declines in real interest rates and a drop in equity valuations. Analysts predict that US and global equities will find a bottom and US rates will peak in the coming year. Alternative investments may enhance cash yields, and real economic growth is entirely determined by innovation. Investors seeking a yield in excess of the market return are looking to invest in illiquid investments such as private equity, private debt non-bank corporate financing, venture capital, and infrastructure investments.

- Inflation is beginning to moderate, but core personal consumption expenditures (PCE) is likely to remain high at around 3%. The Fed is expected to continue to tighten aggressively, with another 100 bp of hikes by the end of Q1 2023. Goldman Sachs Global Economics Analyst Exhibit 4 shows the boost from the rebound in real income vs. the drag from financial conditions. The US GDP growth impulse from GS FCI, 2.0, is projected to grow by 2 percentage points over the next year. Job openings surged in 2020-2021 as employers sought to keep up with the strongest economic recovery on record.

- Central banks in the CEE region are facing a major dilemma next year, with the Czech National Bank and the National Bank of Hungary in the race to start a rate hiking cycle. Inflation in the eurozone has touched 10% Year-on-Year, but CEE is leading the way for two reasons. The global economy is expected to grow at a below-trend pace of 1.8% in 2023, with a mild recession in Europe and a bumpy reopening in China. The US is narrowly avoiding recession as core PCE in ation slows from 5% to 3% in late 2023.

- The market is oversold, with loans trading at $93 and a yield to maturity of around 9.4%. Investors are watching whether the prices and yields on loans are compensating for the heightened recession risks. Reardon Institutional Portfolio Manager, High Yield, expects to see a shift in focus toward slowing global growth in 2023. In high yield, corporate fundamentals still appear to be somewhat resilient. 2022 was a volatile year for equities, with higher inflation and interest rates putting downward pressure on valuations. The Treasury market has endured extreme volatility in the past year.

- The economy is proving too resilient, causing the “looming collapse” in earnings to remain elusive for yet another quarter. Fed policy will continue to be the key driver of asset prices in 2023, with the potential to cut back earnings, increase default risks, widen credit spreads, and increase the chances for a recession. The Bloomberg US BMA6040 Index rebalances monthly to 60% equities and 40% fixed income. Inflation is set to hit 2% by the end of the year, according to the ING global economic outlook for 2023. The US Federal Reserve is prepared to respond to the recession and sharply lower inflation.

- The global economy is on the brink of recession, with central banks raising policy rates to reduce inflation, an energy shock in Europe, and zero-Covid policies in China. Investors must focus their resources on sustainable long-term growth, such as green hydrogen, restoring natural capital, and building green infrastructure. The U.S. stock market remains the focus, but its technology bias and greater sensitivity to interest rate movements may lead to greater investment risks. Inflation is expected to drop due to base effects and lower demand, while shelter costs will eventually reflect the ongoing slowdown in the housing market.

- The global economy is facing a high risk of overlapping shocks due to the COVID shock, which caused US equities to drop less than 10%. The US is pursuing multiple issues at the same time, including monetary tightening, strategic competition with China, and isolating Russia. US employment has only grown 0.7% since early 2020, and inflation has surged worldwide. The yield curve is signaling a potential recession, but the nearterm outlook is one of rising US employment and falling inflation. The world of multilateralism and strong mutual trust between countries and governments ended in 2022.

- In December 2022, CIO Insights Resilience versus recession was released to assess the resilience of Asian economies in the Year of the Rabbit. India, Indonesia, and China, three of the four most populous economies on earth, are expected to grow by 5-6% in 2023. The US Federal Reserve Fed started to hike rates earlier than the European Central Bank ECB, which is facing higher inflation and greater uncertainty regarding energy prices. In EM, the realized default rate is expected to increase modestly to the historical average of 5%. Equity valuations have been under significant pressure due to higher central bank rates and real yields.

- 2023 Outlook 3 2023 economic and market forecasts are based on an average % change from the same period a year ago. U.S. GDP is expected to grow after midyear, but the moderate recession that we anticipate to come first is the main driver behind our forecast for a contraction. Global GDP and Inflation are GDP-weighted averages for developed and emerging economies, and Bloomberg and Wells Fargo Investment Institute have released forecasts for 2023. Goldman Sachs predicts that US growth will remain at roughly this pace, while India’s growth is not expected to be as high as US growth.

- The Federal Reserve Board, Haver Analytics, and Apollo Chief Economist have released data as of October 31, 2022. Central banks are expected to pause rate hike campaigns once the damage becomes clearer, but long-term drivers of the new regime will keep inflation persistently higher. Exhibit 14 shows that it could take two years for inflation to return to 2%. The Fed has been laser-focused on cooling down the economy, but the probability of recession over the next 12 months is already above 50%. Inflation in the services sector, which accounts for roughly 80% of GDP, has been stubborn.

- Inflation is expected to remain high in the coming years, with the ECB’s 2% target in 2024. Labour markets are crucial for the outlook for core inflation, with firms having an incentive to ‘hoard’ staff more than in past recessions. Climate change and the transition to net zero are pushing up costs for energy and commodities, and extreme weather points to more volatility. Interest rates are expected to be the main driver of housing market activity next year. October data from Redfin showed year-over-year changes in rents growing at the slowest pace in over a year.

- Inflation is at a 40-year high, and the Federal Reserve’s interest rate hiking cycle has resulted in negative returns for most asset classes. Will 2023 be any better? Inflation appears to have peaked, which will eventually enable central banks to slow the pace of rate hikes. However, risks have shifted to the lagged impact of aggressive monetary policy tightening on economic growth and earnings. We see a 70% probability of a global recession, but it is likely to be mild and short-lived. Inflation is a key theme for 2023, with higher inflation persisting and sharp rate hikes as a risk.

- The 2023 Investment Outlook for fixed income markets is expected to be driven by the Federal Reserve’s pivot to a less aggressive monetary policy. Jim Caron will take on a new role as Co-Chief Investment Officer, Co-Deputy Head and Senior Portfolio Manager of Global Balanced Risk Control GBaR in January 2023. The global economy is facing a challenging outlook for 2023, with central banks easing off hiking rates as growth slows. Earnings estimates for 2022 and 2023 have barely budged, and valuations have fallen. Fidelity International Equities Marty Dropkin and Ilga Haubelt head of Equities, Asia Pacific and Europe respectively.

- Real rates have been positive for some time, pushing some parts of the yield curve towards pre-Global Financial Crisis GFC levels. This could limit central banks’ ability to support growth with monetary stimulus. The Fidelity International Financial Conditions Index Chart 1 shows that financial conditions have tightened globally, with 105 104 103 102 101 100 99 Jan 2022 May 2022 US EA Sep 2022 UK. Inflation is likely to moderate, but structural trends such as decarbonisation, deglobalisation, and the process of dealing with high debt levels are likely to keep up the inflationary pressure.

- Equities are expected to remain the best-performing asset class over the long term, as they provide ownership in the creativity, ingenuity and productivity of hundreds of thousands of talented workers. Non-fundamental factors such as a stronger dollar and higher energy prices have been driving performance over the short-term. Inflation is too early to tell if it has peaked in the U.S., but there is a lowering of input costs that should improve margins. Hedge funds that use futures and OTC derivatives, complemented with cash related instruments, see their return potential lifted by higher cash rates.

We can further parametrize these to provide even shorter/longer summaries (at the risk of more information loss/gain), here is an example of two shorter summaries, corresponding specifically to Bonds and Interest Rates:

Photon Result (aspects = Bonds, length of 379 words):

- Citi Global Wealth is recommending that investors increase duration before considering lower-quality debt at this stage in the cycle. Yields have soared to pre-financial crisis levels, and the Fed funds rate is likely to be around 4.5% by the end of 2022. Short term bonds offer a better opportunity to lock in peak interest rates, and skilled bond picking managers may be best placed to exploit the wide dispersion in the best and worst performing bonds. In the public markets, managers with flexible capital may be rewarded for their flexible capital, allowing them to evaluate financing solutions across the continuum.

- Citi Global Wealth is looking to capture elevated investment grade credit yields, which are at levels that meet investor goals without the need to extend duration or move down in credit quality. Markets are expecting a recession in 2023, with employment remaining strong and nominal growth expected to be positive. Energy security is vital, and digitization and the growth in alternative investments are redefining real estate. Citi is also looking to boost portfolio immunity with healthcare. The global economy is adapting to the new order, with new energy, labor markets addressing shortages and technology advances limiting cost.

- Bond markets are already pricing a 5% Fed funds rate for Q1 2023, and investors are comfortable with the yield level of short-to-medium and highly rated bonds, which are overweighted. They are also used for diversification purposes, as their correlation with equities typically drops in times of slowing economic growth. Hedge funds benefit from high volatility, diverging fundamentals, and rising income on cash balances. DM Financials are moving up the capital structure, to Tier 2 and Senior debt, which offer attractive yields. Investors who worry that policy rates could go higher can add floating rate notes.

- In 2022, investors closed the books on the year with negative returns, with equity and bond benchmark indexes posting deeply negative returns. The bond market has never posted three consecutive years of negative returns in a row, a feat not seen since 1958-59. Robert Arnott predicts a recession, recovery, and rebound in the first half of 2023, with high-yield bonds offering attractive long-term value. In response, BlackRock Investment Management (Australia) Limited ABN 13 006 165 975 AFSL 230 523 (BIMAL). B’December 2022\n\n2023 Outlook.

Photon Result (aspects = interest rates, length of 268 words):

- Investing in small- and mid-cap companies involves additional risks, such as limited liquidity and greater volatility. Fixed-income securities, including municipal securities, are also subject to market, interest rate, credit, liquidity, inflation, prepayment, extension, and other risks. Bond prices fluctuate inversely to changes in interest rates, and high-yield securities are considered speculative and involve greater risk of default. The US Federal Reserve recently instigated its fastest set of interest rate increases ever, and the resulting higher interest rate environment has left certain yields looking attractive.

- ESG (Environmental, Social, and Governance) factors are not a guarantee of better investment performance. In the 2023 investment outlook, strong fundamentals are offsetting capital market weakness for high-quality assets. On the horizon are more dynamic and highly leveraged markets, ESG retrofit opportunities, and arbitrage between public and private markets. The Federal Reserve has concluded that it is now time to move in smaller increments, but the market doubts their intent. Interest rate changes could also have an impact on investment valuations, and political risks could limit public initiatives.

- Data as of October 31, 2022 shows that US interest rates are expected to rise to around 4.5% in the first quarter of 2023, while the ECB is expected to pause at 2.5%-3.0%. The Bank of England may take longer to reach a peak, given that inflation is likely to be stickier in the UK. Job vacancies are still exceeding the number of unemployed in all major regions, and will be a key indicator to watch in the coming months. Forecasts are based on four-quarter growth in whole-economy total pay in Q4.

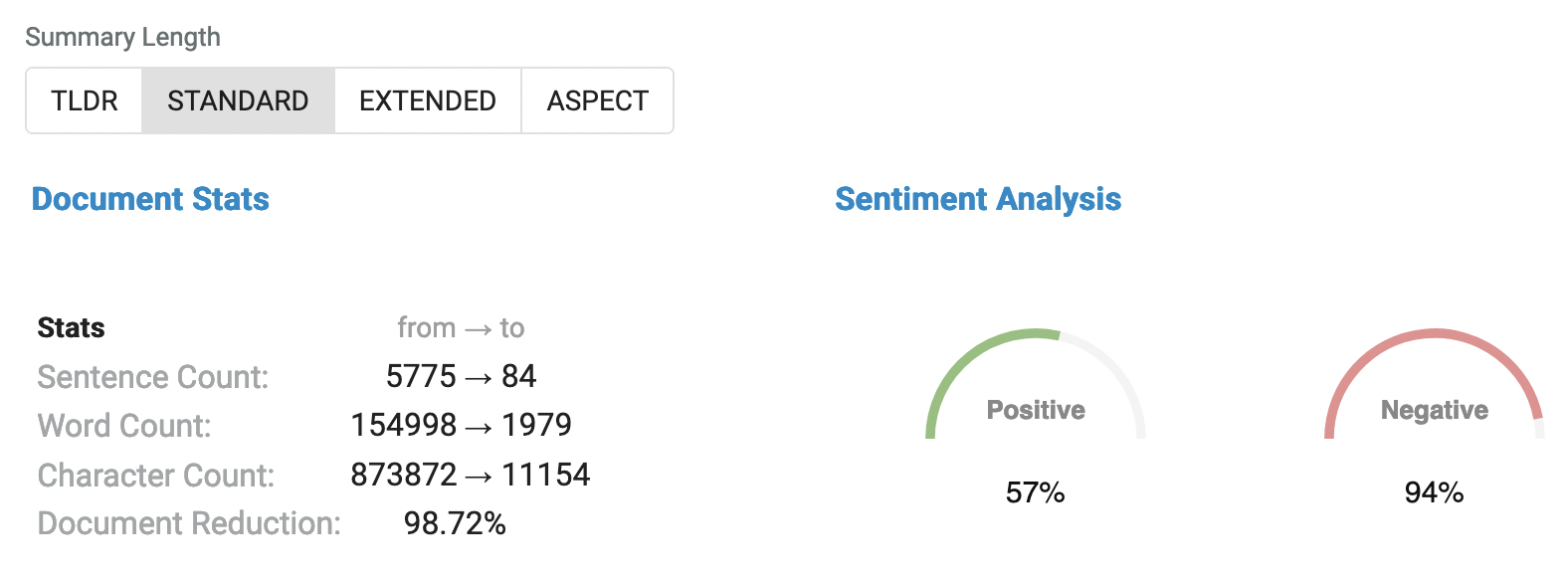

And finally, here is an example of a “regular length” unified summary (corresponding to all the documents), 2000 words explaining the essence of the large set of information.

Photon Result (aspects = ALL, standard length)

- The housing market downturn, triggered by rapid increases in mortgage borrowing costs, is having a ripple effect on the construction sector, which accounts for around 4% of GDP. The Conference Board’s US CEO confidence index is at its lowest level since the Global Financial Crisis 13 years ago, and inflation is set to hit 2% by the end of the year. October data from Redfin showed year-over-year changes in rents growing at the slowest pace in over a year, with median US asking rents dropping below $2,000 for the first time in six months.

- Investors are increasingly asking for more compensation due to the economic downturn, and companies are refinancing debt at lower yields. Central banks are unlikely to come to the rescue with rapid rate cuts in recessions, and investors are advised to take some interest rate risk and are underweight in equities. Investors in a portfolio of 60% global equities and 40% government bonds have lost an eye-watering 20% by late October. Investors are now turning more constructive on corporate credit, particularly highergrade credit in Europe. The Fed’s rate hikes are starting to cool the economy via three transmission channels.

- The Federal Reserve believes that in 2023 it may have a window to tame inflation by keeping policy rates higher for longer, which could benefit economic growth and asset valuations. In January 2023, Jim Caron will take on a new role as Co-Chief Investment Officer, Co-Deputy Head and Senior Portfolio Manager of Global Balanced Risk Control GBaR. Fixed-income securities are subject to the ability of an issuer to make timely principal and interest payments credit risk, changes in interest rates interest-rate risk, the creditworthiness of the issuer and general market liquidity market risk.

- The United Kingdom’s departure from the European Union and European Economic Area has been designated as “Brexit Day” and the following information with respect to distributing entities will apply. Goldman Sachs International “GSI” is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority, and has approved research in connection with its distribution in the United Kingdom. GSI – Sucursal en Espa a Madrid branch has been authorized in Spain by the Comisi nacional del Mercado de Valores, and Goldman Sachs Bank Europe SE “GSBE” is a credit institution incorporated in Germany.

- The high-yield bond market has mostly shut down for new issuers, and the era of low rates seems over. SP Global Ratings Research, Apollo Chief Economist, has released data as of July 1, 2022. The global government bond benchmark has seen yields rise by roughly 200 basis points since the start of the year. The drawdown in the Bloomberg Barclays Global Bond Aggregate in the first 10 months of 2022 was four times as bad as the previous worst year since records began in 1992. Inflationlinked bonds are overweight, while European government bonds are underweight.

- The UN expert group has reported that one-third of the world’s largest publicly-traded businesses have made net zero commitments, and only half of those show how their targets are embedded in their corporate strategy. External pressure from customers and non-governmental organisations will drive more companies to make commitments or adjust their current targets. The World Bank data shows a gap of $15 trillion between existing investments and what is needed to meet global infrastructure demand. The U.S. Inflation Reduction Act alone earmarks nearly $400 billion of investment and incentives in sustainable infrastructure and supply chains.

- 2023 Investment Outlook is underpinned by post-COVID recovery, manufacturing revivals, and the “China plus one” strategy. Commodity boom is driven by resource-intensive decarbonization, which benefits resource-rich economies. EM equities are trading at crisis-level valuations, and ESG Strategies that incorporate impact investing andor Environmental, Social and Governance could result in better performance. Global Macro is expected to benefit from inflation, a still-strong dollar, higher interest rates, and heightened market volatility in 2023.

- Citi Global Wealth Investments is a global asset management company that specializes in global diversified portfolios for the long term. In August 2008, the cash-heavy allocation would have returned only 21%, compared to 50% for the AVS Risk Level 3 allocation. However, after this point, both began to recover and reached breakeven in 20 and 13 months respectively. Forecast 10-year returns have risen across all asset classes, but many investors are sitting on excess cash. In 2022, a rare simultaneous selloff in equities made it difficult for many investors to generate small gain in nominal terms.

- Inflation is still at a multi-decade high, with 70% expected to peak by the end of 2023. The US Federal Reserve is likely to hold rates steady after its final hike, with the fed funds rate likely to peak around 5% by the middle of next year. The Fed increased interest rates another half percent to a target rate of 4.25% to 4.50% in December. US labor markets are more competitive than in the 1960s-1980s period, but many Fed policymakers fear inflation will develop “a life of its own” and persist beyond the initial sources of instability.

- The 2023 Equity Sector Outlook is expected to be balanced and ready, with the Energy sector being favored. Supply chains are expected to remain unbalanced due to shifting trade patterns due to sanctions on Russia and geopolitical tensions. Logistical bottlenecks started to subside in 2022, but the recovery of schedule reliability will take us far into 2023. The ING global economic outlook for 2023 is 2023 December 2022, with lower transport costs for overseas container trade. China is facing a supply-chain integration process that has expanded to include Asia. Oil and gas companies have been the major beneficiary of high commodity prices.

- Inflation is having a negative impact on investments, and can lead to a real loss in value. Economic development beyond 2023 is likely to depend on success in commercialising new technologies and integrating them in the economic cycle. Inflation has become a dominant topic again, with Germany, 8.9% in Germany and 8.4% in the Eurozone. The ING global economic outlook for 2023, 2023 December 2022, is expected to show both headline and core inflation above 3%. The European Commission’s proposal to build in more flexibility and practice a more tailor-made and country-specific approach is being considered.

- The 2023 outlook for investors is a recession, recovery, and rebound. Equity and bond benchmark indexes posted negative returns this past year, a double dose of disappointment unmatched over the past 50 years. High inflation and the end of pandemic-related transfer payments reduced real disposable income in 2022, but real spending growth remained more resilient. Inflation is a growing concern for investors, with consensus forecasts underestimating how high it would go. Central banks are pausing rate hike campaigns, and long-term drivers of the new regime are expected to keep inflation persistently higher.

- The correlation between bonds and equities has been strong, with the RHS 0.6 0.4 ISM index 60 0.2 0 55 -0.2 50-0.4. Yields have reached levels that offer some protection against adverse market effects, and the diversification benefits of adding bonds to a portfolio are expected to return. BNY Mellon Wealth Management has a cautious positioning with a neutral weighting in equities, a small underweight in fixed income, and a small overweight to less correlated diversifiers.

- The U.S. stock market is expected to remain the focus in 2023, with stocks expected to grow in the single-digit percentage range. Investors are advised to invest in companies with high quality, franchise businesses, recurring revenues and pricing power. Central banks are attempting to counter inflation through higher rates, while Indian stock markets have performed well despite volatility. The 2023 SP 500, Germany DAX Eurozone, Euro Stoxx 50, Japan MSCI Japan, Switzerland SMI, U.K. FTSE 100, and Asian markets remain attractive.

- Central banks are tightening financial conditions, increasing the risk of an inflation bust across a glut of economies. This has been good for bonds, but there are the first signs of cracks in financial systems. The Federal Reserve is pressing on with tightening, which has turned the dollar into a 2%. Inflation is likely to be the key to this, with the US and Europe facing high inflation. The global economy is undergoing a fundamental reset, with central banks expecting the fastest pace of tightening on a 12-month basis.

- The Russia-Ukraine situation has improved, avoiding a deep recession. The housing market has cooled and capital spending has rebounded with confidence. Unemployment rates remain low, and the Federal Reserve has increased rates to around 5%. The Bank of England has a peak UK interest rate of around 4.5%. Central banks are forced to tighten policy more than in the central scenario to anchor inflation expectations. Inflation is expected to ease through the course of 2023, with the shrinking contributions from energy and goods sectors in particular helping price pressures to moderate. Job vacancies are still too hot, with US interest rates rising to 4.

- BNY Mellon Wealth Management has forecast a mild recession in 2023, with stocks and bonds offering attractive opportunities. Inflation is elevated above the post-global financial crisis level, and the Federal Reserve is likely to hike and hold due to elevated inflation. Citi Global Wealth OverVIEW 16 Investments looks at long-lasting income-producing assets in Europe, Japan, and others at unusually depressed values. Germany’s REITs have returned negative 40% in 2022, but if Europe were to recover half of its losses of the past two years, the annualized return would be 19%.

- The advance GDP report showed 2.6% annualized growth in Q3, with nonfarm payrolls growing 261k in October. Goldman Sachs Co. LLC investors should consider this report as only a single factor in making their investment decision. The IMF forecasts used for India for 2023 and 2024 are the long-run estimate for the US, Japan and Canada. The global private banking industry is expected to grow in 2023, with earnings resilience and yields being a risk. Global economic momentum is slowing, with the Eurozone and UK in recession and China’s 2023 recovery likely to be shallow.

- Inflation is expected to decline from 5.1% in September to 2.9% in December 2023, according to the University of Michigan Survey, next 5-10 years. Supply-constrained durable goods with still elevated margins, such as used cars, are expected to drive nearly half of the slowdown in overall core in ation. In November 2022, Goldman Sachs Global Economics Analyst Exhibit 8 shows the disinflationary impact of normalizing supply chains and rental markets. The recession is reducing demand for an array of goods and services, and inflation for “stickier,” less economically sensitive prices excluding housing was back down to a December 2021 low.